-

Get the latest news! Subscribe to the ifa bulletin

Get the latest news! Subscribe to the ifa bulletin

Powered by

MOMENTUM

MEDIA

The Australian Taxation Office (ATO) allows investors to choose between two methods of claiming depreciation on the plant and equipment assets within their investment properties. These are the diminishing value and the prime cost methods of depreciation.

Every property investor is likely to have a different investment strategy, so it is important for Property Managers to have an understanding of how choosing between the two different methods of claiming depreciation will affect their client’s cash flow.

The diminishing value and prime cost methods both claim the total depreciation value available over the life of a property. However, the two methods use different formulas to calculate depreciation deductions, achieving different short and long term cash flow positions for the property investor.

Legislation allows property investors who use the diminishing value method to increase the rate an asset depreciates at, therefore increasing deductions sooner. This method calculates the depreciation based upon the reduced written down value remaining so the deduction diminishes over time. The prime cost method uses a lower percentage rate of depreciation and results in a consistent deduction per year, spreading the deductions out more evenly over time.

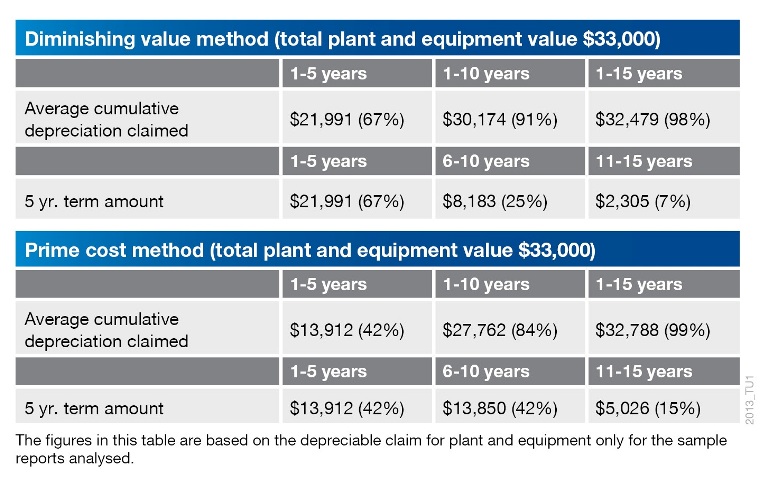

To investigate how the outcome varies over a five, ten and fifteen year period for both methods, a sample of BMT Tax Depreciation Schedules was analysed for properties which contained assets totalling $33,000 in value.

The following table shows a comparison of the depreciation claimed over time, as they accumulate and in five year blocks.

The analysis found that:

As the example shows, investors who choose the diminishing value method claim greater depreciation deductions in the earlier years of owning the property. From the sample we can see $21,991 in depreciation deductions were claimed using this method by comparison to $13,912 using the prime cost method in the first five years. If an investor is only planning on holding a property for a shorter period of time, they wish to build their investment portfolio quickly or they want to save quickly to budget for a renovation to the property, this method might be their preference.

Alternatively, the prime cost method benefits those who prefer to claim consistent deductions over a longer period of time. In the sample, those choosing this method were be able to claim higher deductions in the eleven to fifteen year period, claiming $5,026 compared with only $2,305 using the diminishing value method.

A property investor can only use one method to claim depreciation deductions. Once an investor chooses the depreciation method used for an asset, it cannot be changed. Property Managers should encourage investors to discuss their individual situation with an Accountant and a Quantity Surveyor who can provide further information on depreciation and these methods.

Never miss the stories that impact the industry.

Get the latest news! Subscribe to the ifa bulletin